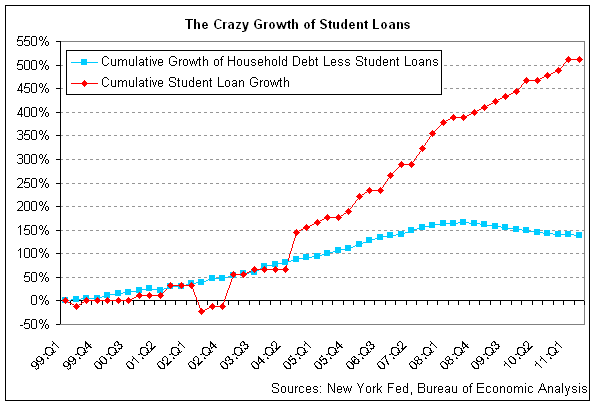

American student loan debt grew 511% between 1999 and 2011. It now totals over $1 trillion, a collective finanical burden that rises well above auto loan and credit card debt, (which total around $783 and $679 billion, respectively.)

With college tuition costs growing an estimated 10 times faster than housing, health care and food costs, what’s to stop its march towards the heights of mortgage loan debt, which toppled $8.48 trillion as of March 2013?

While hopeful students continue to enter college and take out larger and larger loans to pay for their education, a record number of student loan borrowers defaulted on their loans last year.

This year, we’ve seen Mutual Aid in Motion.

From scaling sharing hubs to Mutual Aid 101 trainings, we’re helping communities build the tools they need.

Every dollar fuels lasting resilience – proving that when we move together, we all move forward.

Is student loan debt smart? And more to the point, how is this model sustainable? Student loan expert Anya Kamenetz says no. The student loan crisis is a bubble with an inevitable pop—but nobody seems to know what exactly the pop will look like. (Her interview below.)

As a college grad and student loan debtor, I find all of this information both relevant, and full of red flags. What is debt-subsidized education doing for the future of the country? And what makes all of us buy in?

Quite clearly, it isn’t realistic to expect that all $1.8 million college graduates each year (not counting the 1 million Masters and Doctorates) will find an income proportionate to the loan debt that saddles them right out of the gate.

So if the fleeting grace period ends and $288 monthly loan payments suddenly appear much larger than they’re supposed to… What then? And more importantly, how do we keep our children (should we ever afford them) from having to go into debt in exchange for a college education?

Anya Kamenetz, a journalist, student loan expert, and author of the book Generation Debt, will host a live, interactive webinar called In Debt We Trust: Student Loans And the Rest of Your Life that starts on August 7 on Evolver Learning Labs.

The three-part webiner is an invitation for debtors to “stop suffering alone in silence,” and start talking about the debt that ails them—an experience which Kamenetz says is not unlike an “accute personal catastrophe” should the loan go into deliquency or default. The webinar will illuminate the options, from the "practical to the radical," and talk about the possible alternatives to an education system anchored in debt.

Kamenetz will interview one of the following experts over the next three Wednesday evenings, before opening the webinar up for questions and discussion: Heather Jarvis, student loan expert, Thomas Gokey, artist, activist with Strike Debt and author of Poopsicle Story and Charles Eisenstein, author of Sacred Economics, who will get into the more spiritual aspects of debt—how debt fits into a core condition of the economic and social reality of the American culture, what it means psychologically, and how to move away from a world of scarcity and into a world of abundance.

Before I signed up for the webinar, I interviewed Anya Kamenetz:

How did your interest in the student loan crisis come about nine years ago?

I was originally assigned the topic by my editor at the Village Voice. Like any reporter I got interested in covering a story that was complex and also had a very human face.

Why do you call the student debt situation a "crisis"?

I call it the student debt crisis because education is fundamental to our progress as a society, yet ever-increasing tuition and debt financed education undermines social mobility. Heavy loans put a penalty on academic striving, detracting from the achievement and advancement of smart, ambitious people, who should be our greatest asset. People in delinquency or default really face acute personal catastrophes.

It's interesting that you began as a reporter, but now you are somewhat of an expert, and in some ways, it seems, a therapist. Obviously you've made yourself into an expert on the many facets of the situation — have you found many others who are like you in this way?

Every time I publish an article on some aspect of the student loan crisis I hear from several people in need of help. I try to refer them to others who are qualified to help like the Project on Student Loan Debt, Student Loan Justice, and Heather Jarvis who maintains the website askheatherjarvis.com.

In one of your recent articles, you say that young people who take out loans are "investing in themselves." The phrase rang true for me. I did the same, and I pictured myself making much more money after graduating. Would you say that the student loan system fails to alert borrowers that their future selves may not make even close to enough money to pay off the loans they are taking out? How do you think they might be able to better illustrate the reality of the situation?

I think you've put the finger on the problem–it is all about hope. We don't want people to do a cold cost-benefit analysis when they are quantifying their future dreams. But someone has to introduce some sanity into the system. If I had my way I would have every student sit down with a counselor and review the job opportunities and salaries available in their future fields before making the decision to go into debt.

You say that the student loan debt simply can't, realistically, go on like this. Can you explain what you mean and how you think it might end? What are the alternatives?

If you look at the graphs of student loan debt since the 90’s , and college tuition since the 70’s , they resemble the graphs of the cost of houses and the rise of mortgage debt pre-crash.

Today the most expensive private university in the country, NYU, costs approximately $244,000 for four years. If current trends continued uninterrupted, a regular in-state public university would cost in 20 years what a private university costs today (approximately $32,000 a year) and an NYU education would cost almost half a million. I just don't believe those trends are sustainable, which is why I think they must be interrupted by some unpredictable event, such as the emergence of ultra-low-cost alternatives.

The upcoming webinar will interview three expert guests. Can you say a little bit about why you chose each one?

Heather has the ability to give practical help and an overview of debt and repayment policy. Thomas Gokey is a creative activist with a record of resisting debt in surprising ways. And Charles Eisenstein has a holistic understanding of the psychological and psychic toll that debt takes on individuals and society.

What can participants in the Webinar hope to gain from participating?

Help with their debt situations, and greater perspective on the process.

I often wish student loan debt could be payed back in volunteer hours. I know this is a rather naive dream, but at the same time it's also irresistible because I think it could really help the world. What would a more realistic solution be?

Australia has a scheme whereby student debts are repaid as a percentage of income. This allows those who have received the greatest material rewards from education, to help shoulder the burdens of others. It's basically a progressive income tax. Something similar has just been proposed in Oregon.

Sign up for the live, interactive webinar here. Follow Maria Grusauskas on Twitter @MariaGwrites and Facebook.